Economy at a Glance - August 2023

The "R" Word Revisited

“Resilient” is a better word than “recession” to describe the U.S. economy, as recent indicators show.

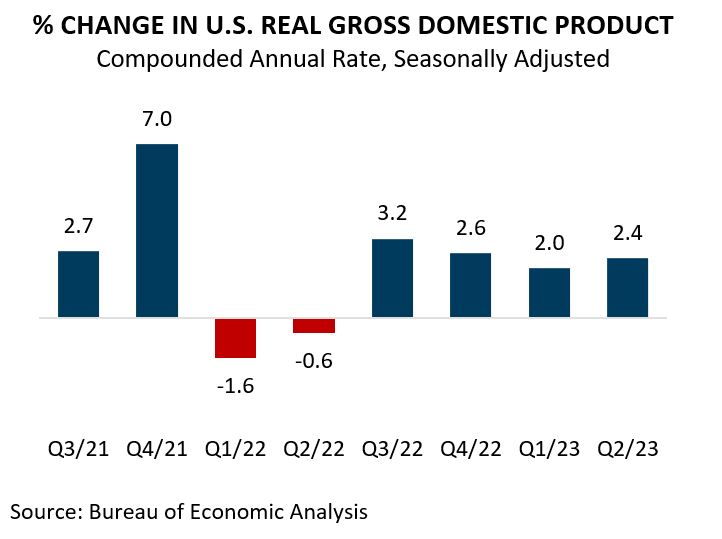

Gross domestic product (GDP) grew at a 2.4 percent annual rate in Q2/23 adjusted for inflation, well above the 2.0 percent that many economists had expected.

Growth was driven by increases in consumer spending (+1.6 percent), business investment (+4.9 percent), and government outlays (+2.6 percent). Drops in exports and new home construction offset these gains, or growth would have been stronger.

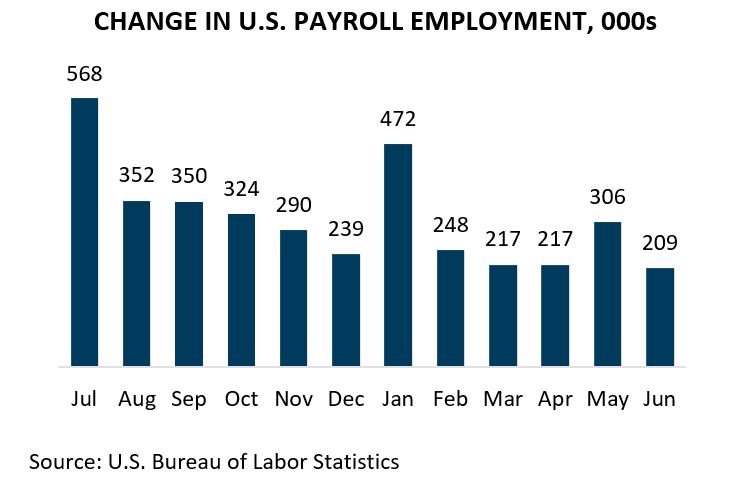

The U.S. added 209,000 jobs in June. Though weaker than in recent months, the gain aligns with the monthly average (189,000) in the years between the Great Recession and the Covid Recession.

Future gains will depend on increases in the labor force participation rate (LFPR) and economic growth. The LFPR was 62.6 in June, an improvement from 61.5 percent last June but below the 63.3 percent prior to the pandemic.

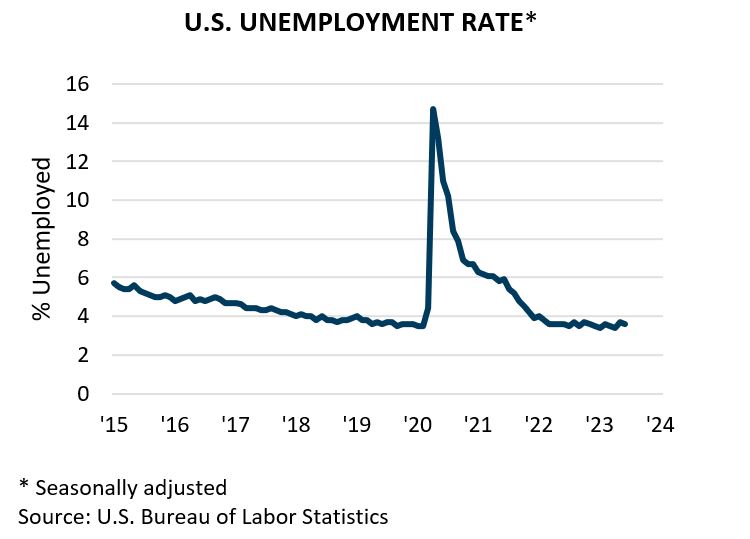

The unemployment rate was 3.6 in June. Any rate below 5.0 suggests a tight labor market. It has tracked 4.0 percent or lower for 19 consecutive months.

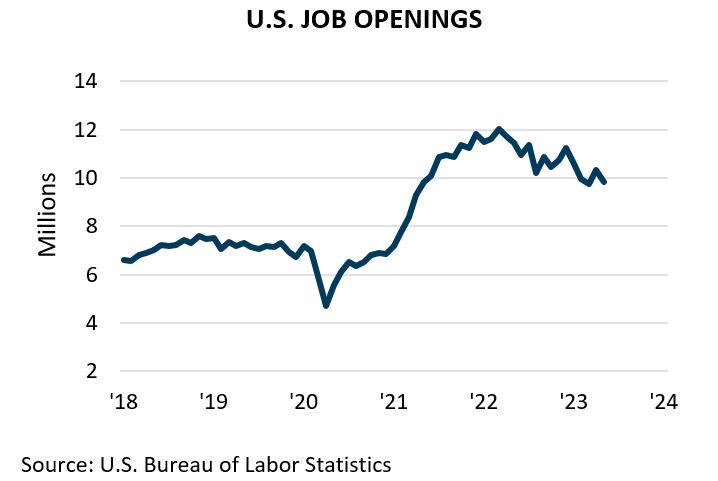

There were 9.8 million job openings in May, down from 11.4 million May ’22 but well above the 6.4 million monthly average prior to the pandemic. These are jobs for which work is available, can be started within 30 days, and the employer is active recruiting for the position.

The tight labor market has boosted wages, offsetting losses in purchasing power due to inflation. Over the past 12 months, average hourly earnings have increased 4.4 percent, according to the U.S. Bureau of Labor Statistics (BLS). Inflation, as measured by changes in the Consumer Price Index (CPI), was 3.0 percent in the 12 months ending June ’23.

The U.S. Federal Reserve may achieve its soft-landing for the economy, i.e., reducing inflation without spiking unemployment. Employers remain reluctant to cut staff fearing they won’t be able to rehire them when demand picks back up. Forty-two percent of respondents to a National Association for Independent Business (NFIB) survey reported they had job openings they could not fill. The difficulty in filling open positions is most acute in the manufacturing, construction, and transportation sectors.

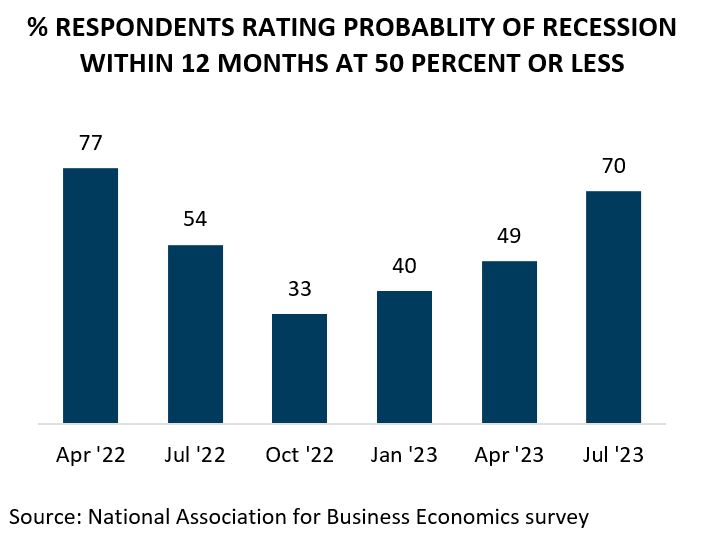

More economists see the U.S. avoiding a recession altogether. Seventy-one percent of respondents to a National Association of Business Economics (NABE) survey rated the probability of a recession over the next 12 months at 50 percent or less. That’s a dramatic improve-ment over the last four surveys.

To continue reading, download this report.

Note: The geographic area referred to in this publication as “Houston,” "Houston Area” and “Metro Houston” is the nine-county Census designated metropolitan statistical area of Houston-The Woodlands-Sugar Land, TX. The nine counties are: Austin, Brazoria, Chambers, Fort Bend, Galveston, Harris, Liberty, Montgomery and Waller.