Economy at a Glance - January 2023

U.S. Economic Outlook

The U.S. economy continues to grow despite rising interest rates, a plunge in new home construction, the ongoing war in Ukraine, concerns over a new COVID variant, and a looming recession in Europe. The long-anticipated recession has yet to arrive.

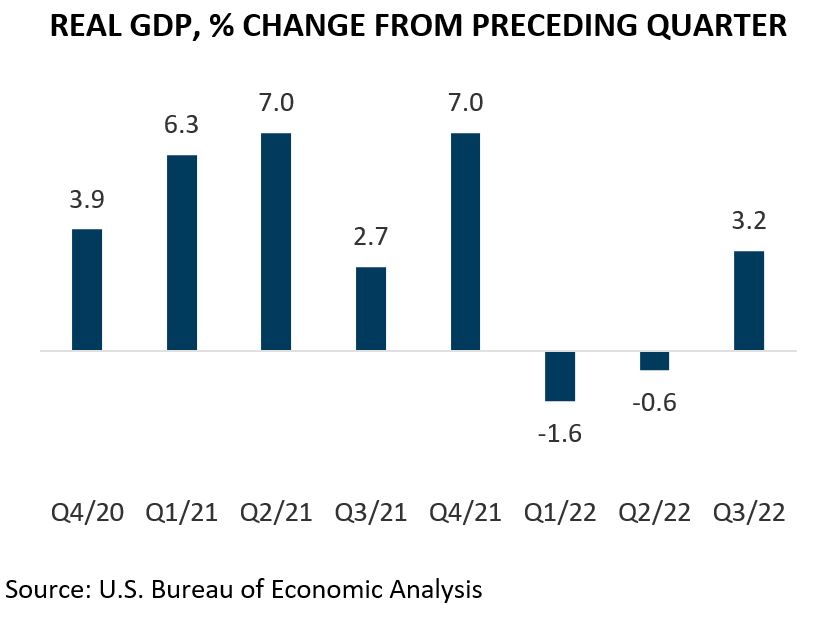

U.S. gross domestic product, the most comprehensive gauge of the nation’s economic health, grew 3.2 percent in Q3/22 adjusted for inflation. That’s up from a decline of 0.6 percent in Q2/22 and a drop of 1.6 percent in Q1/22.

The 3.2 growth rate reflects an upward revision from two previous estimates issued by BEA. Initially, the agency estimated U.S. GDP grew 2.6 percent in Q3, later revised that to 2.9 percent, then revised that to 3.2 percent.

Growth was driven by rising exports, an increase in consumer spending, an uptick in commercial real estate, equipment, and intellectual property investments, and higher state, local, and federal government spending. These were somewhat offset by drops in home construction and inventory purchases.

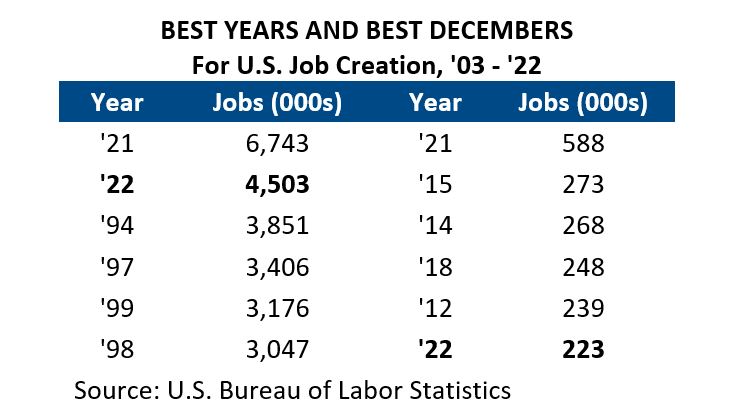

The nation created 223,000 jobs in December, which brought overall growth for ’22 to 4.5 million jobs. That ranks as the fifth-best December and the second-best year on record for job creation in the past two decades.

Nationally, initial claims for unemployment benefits, a proxy for lay¬offs, continue to trend lower. The four-week average slipped to 213,750 the last week of December, down from 249,500 in early August, the most recent peak.

The four-week average for continued claims rose to 1,687,500, from a trough of 1,314,00 in early June. However, continued claims are tracking well below the comparable period in ’21. This suggests it takes marginally longer for laid-off workers to find employment now than in the summer, but less time than it did late in ’21.

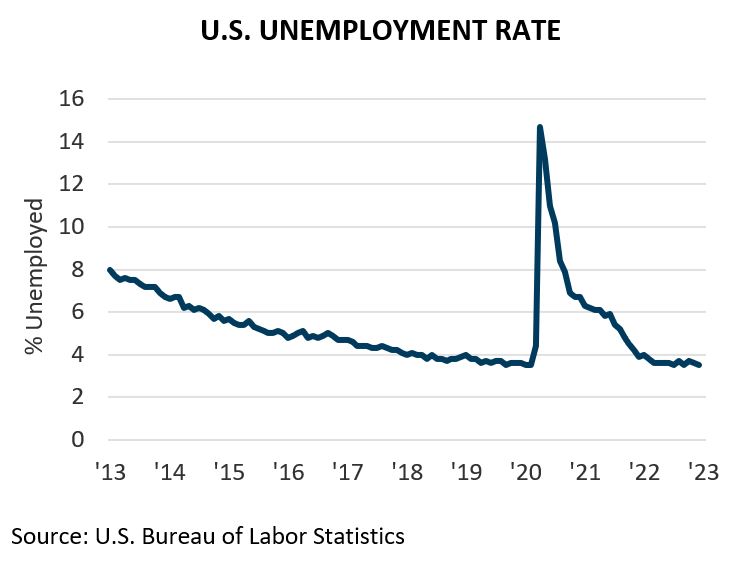

The U.S. unemployment rate (seasonally adjusted) slipped to 3.5 percent in December and has remained between 3.5 percent to 3.7 percent since March ’21. The number of unemployed fell to 5.7 million in December, down from 6.3 million in December the year prior. The jobless rate for adult men was 3.1 percent, for adult women, 3.2 percent; for teenagers, 10.4 percent; for Whites, 3.0 percent; for Blacks, 5.7 percent; for Asians, 2.4 percent; and Hispanics, 4.1 percent.

The labor market remains tight. The Bureau of Labor Statistics (BLS) reports there were 10.5 million job openings on the last business day of November. That’s an improvement from the peak of 11.9 in March ’22 but still above the 6.9 million in November ’19 prior to the pandemic. Nearly 4.2 million workers quit their jobs in November, somewhat above the 3.5 million in November ’19. The high level of quits suggests workers are more easily finding better pay or working conditions with other employers, or they’re confident they will have little difficulty doing so. The strong labor market is one factor driving inflation and influencing the Federal Reserve to continue raising interest rates.

To continue reading, download this report.

Note: The geographic area referred to in this publication as “Houston,” "Houston Area” and “Metro Houston” is the nine-county Census designated metropolitan statistical area of Houston-The Woodlands-Sugar Land, TX. The nine counties are: Austin, Brazoria, Chambers, Fort Bend, Galveston, Harris, Liberty, Montgomery and Waller.