Economy at a Glance - March 2023

Subtle Shift

There’s been a subtle shift in the narrative on the U.S. economy in recent weeks. In February, The Wall Street Journal ran a front-page article under the headline “Hard or Soft Landing? Some Economists See Neither if Growth Accelerates.” The article noted:

Surprising strength in hiring and consumer spending along with signs that demand for autos and housing are stabilizing have some economists pointing to a third scenario that seemed improbable at the start of the year—an economic growth upturn.

The New York Times published a similar story under the headline “What Recession? Some Economists See Chance of a Growth Rebound.” Per the Times article:

After months of asking whether the Fed could pull off a soft landing in which the economy slows but does not plummet into a bruising recession, analysts are raising the possibility that it will not land at all — that growth will simply hold up.

And under the headline “Forget Hard or Soft Landing: Meet the Rolling Recession,” Bloomberg took a different slant:

...one industry suffers a contraction, then another, but the economy as a whole never swoons, and the job market largely holds up.

Bloomberg cites the downturn in housing and the current spate of tech layoffs as proof points for a rolling recession.

Much of the economic news supports the possibility that a recession can be avoided.

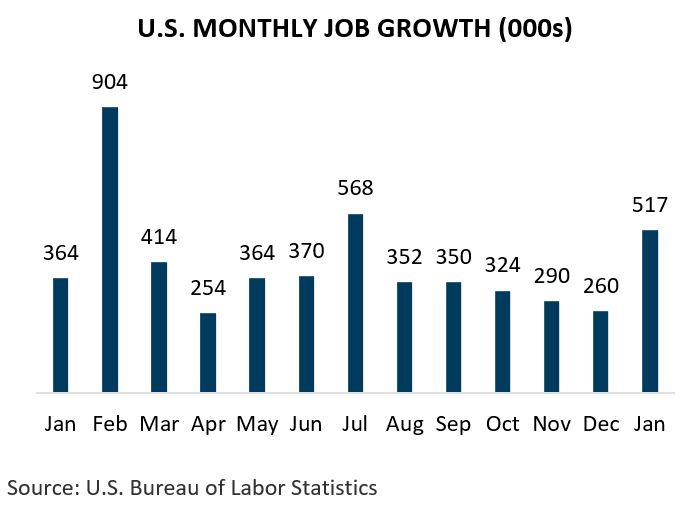

- Job growth remains robust. The U.S. added 517,000 jobs in January, more than double what economists forecast.

- Unemployment remains low. The rate fell to 3.4 per-cent in January, the lowest since May 1969.

- The labor market is tight. U.S. employers had 11.0 million open positions in December, well above the 6.5 million average in the years prior to the pandemic.

- Despite a rash of tech layoffs, there’s been no surge in initial claims for unemployment benefits. The four-week average fell to 189,500 in mid-February, down from 209,000 for the comparable period in ’22.

- Consumers continue to spend. U.S. retail and food service sales for January topped $697.0 billion, up 3.0 percent from the previous month.

- Factory activity has picked up. New orders for manufactured goods rose $10.0 billion or 1.8 percent to $552.5 billion in December. Orders have risen four of the last five months.

- And the housing market is recovering. Sales of new single-family homes hit a seasonally adjusted annual rate of 616,000 in December, 2.3 percent above the November estimate of 602,000.

Not all the news is positive, however.

- New home construction remains weak. In January, housing starts fell 4.5 percent compared to December.

- Overall construction is down. Total activity for December slipped 0.4 percent below November levels.

- Inflation remains stubbornly high. The Consumer Price Index for All Urban Consumers (CPI-U) rose 6.4 percent in the 12 months ending January ’22.

- Businesses are struggling with increased costs. The Producer Price Index (PPI) rose 6.0 percent in the 12 months ending January ’23.

- And many business leaders have embraced a gloomy outlook. Ninety-three percent of respondents to The Conference Board’s Measure of CEO Confidence survey are preparing for a U.S. recession over the next 12-18 months.

With so many conflicting indicators, it’s no wonder economists can’t agree on the direction of the economy.

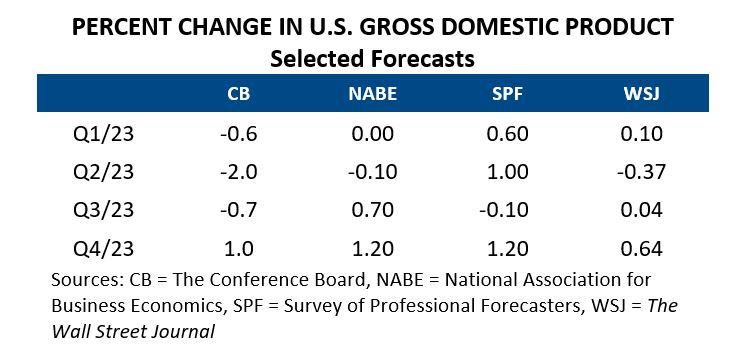

The Conference Board forecasts U.S. gross domestic product (GDP) to contract three consecutive quarters this year.

The National Association for Business Economics (NABE) has GDP flat in Q1, an almost imperceptible dip in Q2, and growth again in Q3.

The Federal Reserve Bank of Philadelphia’s Survey of Professional Forecasters has U.S. GDP declining in only one quarter this year, and even then by only 0.1 percent.

The Wall Street Journal’s survey of U.S. economists has the probability of recession this year at 61 percent. The Journal forecasts a mild contraction in Q3 with growth resuming in Q4.

What’s hidden in the detail of the Journal’s survey is that one-fourth of the respondents don’t expect any decline in ’23. This includes economists at well-respected firms like Credit Suisse, Goldman, Sachs, Morgan Stanley, the National Association of Manufacturers, National Association of Realtors, Northern Trust, and Societe Generale.

This lack of consensus may be why The Washington Post published an opinion piece in late February with the headline “Don’t Believe What Anyone Says About the Economy. Even Me.” The article notes:

- Current economic data is confusing because it points in all directions.

- The confusion is fertile ground for partisans who use the data to serve their own agendas.

- How one feels about the economy depends on one’s personal situation, i.e., good data is cold comfort to someone who lost their job or whose business is being strangled by inflation.

So what does the Partnership make of the data?

- Given the tight labor market, a recession is still possible but less likely.

- Inflation remains stubbornly high, so the Fed will keep raising interest rates.

- The Fed’s actions will have the greatest impact on rate-sensitive sectors of the economy. Construction will wane. Property owners will struggle to service their debts. Loan defaults will escalate.

- The drop in labor force participation and lack of a coherent immigration policy will prolong worker shortages.

- Barring a “black swan” event, the U.S. and Houston economies will continue to grow this year.

To continue reading, download this report.

Note: The geographic area referred to in this publication as “Houston,” "Houston Area” and “Metro Houston” is the nine-county Census designated metropolitan statistical area of Houston-The Woodlands-Sugar Land, TX. The nine counties are: Austin, Brazoria, Chambers, Fort Bend, Galveston, Harris, Liberty, Montgomery and Waller.